Bondsavvy has added seven new recommended corporate bonds to buy over the last week: four for our Premier Service and three for our Basic Service. This takes our total number of recommended bonds to 66 for Premier and 13 for Basic.

Highlights of our best individual corporate bonds to buy now include:

- The new Premier Service bonds had pick-date yields to maturity ranging from 5.64% to 6.31%.

- The Basic Service bonds had pick-date YTMs between 5.38% to 5.87%.

- YTMs of six of the seven new bond picks were at least two percentage points higher than current money market yields. Corporate bond coupons are fixed whereas money market yields are not.

- As of 10:00am EDT on July 2, the new bonds were still available at prices at or near the pick date price. The average price changes for the Premier and Basic picks were +0.11 points and -0.26 points, respectively.

- We seek to achieve returns exceeding the pick-date YTM through our active bond investing strategy.

- All of the recommended bonds to buy had investment-grade bond ratings, with the exception of one pick in both Premier and Basic that was split rated (investment grade by one rating agency and below investment grade by the other).

- Maturity dates ranged from 2034 to 2039. Since Bondsavvy subscribers invest in our recommendations through brokerage accounts they control, they have the flexibility to own bonds of different maturity dates than those we recommend.

Our Recommended Bonds to Buy 2026 Preview

Before Bondsavvy, investors seeking the best individual corporate bonds to buy had to sift through over 10,000 corporate bonds available when buying bonds online. Since 2017, Bondsavvy has made bond investing simpler and more profitable by presenting between 15-20 new recommended corporate bonds each year for our Premier Service. We launched our Basic Service in December 2025 so a broader group of investors could benefit from our bond recommendations.

While our 92 previously exited Premier Service recommended corporate bonds skewed toward high yield corporate bonds, 23 of our most recent 31 Premier Service recommended bonds to buy had investment grade bond ratings. All of our Basic Service bonds are investment grade; however, we currently have one bond that is split rated.

Bondsavvy's Premier Service makes new corporate bond recommendations each quarter during The Bondcast, a webinar exclusive to Bondsavvy subscribers. The 66 bonds currently on the Bondsavvy Premier recommended corporate bonds list (including 39 rated buy and 27 rated hold) offer a wide range of maturity dates and are from issuers across over 15 different industry groups.

Bond Pick Updates Coming Soon

Each quarter, we update our buy/sell/hold Premier and Basic bond recommendations with the latest issuing company financials and up-to-date bond prices, yields, and credit spreads. Our next best individual corporate bonds to buy now updates will be:

- July 9: Updates of Premier Service's 66 recommended corporate bonds

- July 14: Updates of Basic Service's 13 recommended corporate bonds

Higher US Treasury Yields Have Improved Bond-Buying Opportunities

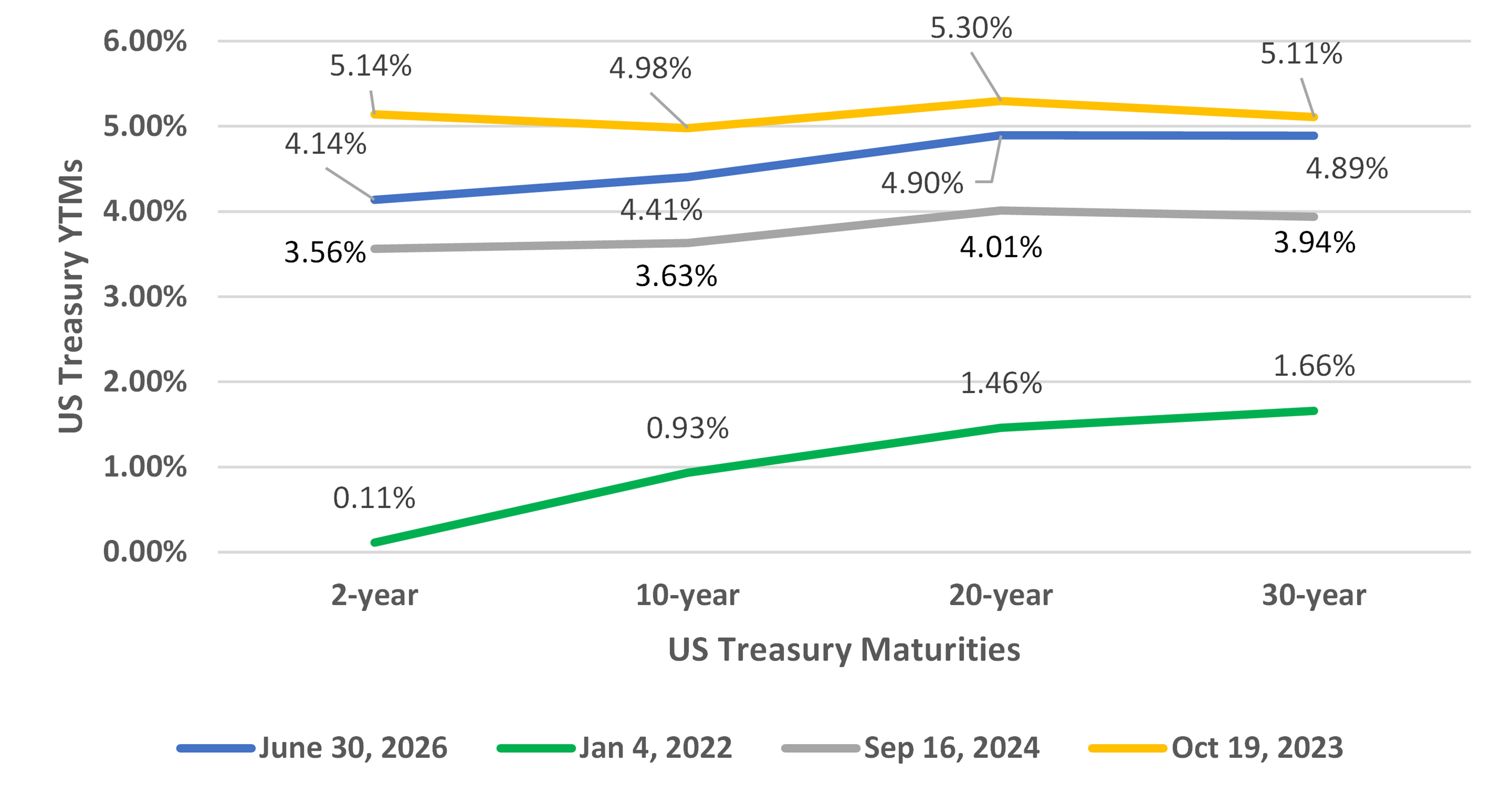

As we discuss in our corporate bond credit spreads blog post, US Treasury yields and credit spreads are the two components of US corporate bond yields. Figure 1 shows four recent US Treasury yield curves, which enable investors to evaluate the value available in the US bond market. Higher bond yields typically mean more bang for your investing buck.

As shown in Figure 1, the recent trough of US Treasury yields was January 4, 2022 (the green line), which came before the US Federal Reserve began increasing interest rates in March 2022. The recent peak US Treasury yield curve occurred on October 19, 2023.

When US Treasury yields are relatively high there is generally greater value available in bonds, as investors are receiving a higher level of income, and bond prices generally have a greater chance of increasing.

Figure 1: Recent US Treasury Yield Curve Comparison 2022 to 2026

Source: Tradeweb data as shown on CNBC.com and graphed by Bondsavvy. June 30, 2026 yields as of 11:30am EDT.

While the US Treasury yield curve on June 30, 2026 (the blue line) was not as high as the October 19, 2023 yield curve (the orange line), the 30-year US Treasury yield was within 22 basis points of the 5.11% high reached October 19, 2023. The lowest bond yields have been over the last two years occurred in September 2024 (the gray line). On June 30, the 10-year US Treasury yield had increased 78 basis points to 4.41% from the September 2024 trough.

Of course, US Treasury yields are only one part of the corporate bond yield puzzle. Changes in corporate bond credit spreads can either magnify or mitigate a corporate bond yield's change.

Why Own Our Best Individual Corporate Bonds to Buy

Owning individual corporate bonds enables investors to lock in high income for a specific time period and to

have the opportunity for capital appreciation. Individual corporate bonds also, at maturity, provide for a return of

the $1,000

face value for each bond you own. That said, we seek to achieve corporate bond returns that exceed a bond's pick date yield to maturity by using our active bond investing strategy.

Since corporate bonds are priced as a percentage of their face value, investors can evaluate a bond's price, YTM, and

credit spread and compare these metrics to the

bond issuer's financials. This financial analysis is the heart of the Bondsavvy investment service and enables us to identify bonds that can achieve

strong total returns over the long term. This analysis is not possible when investing in bond funds and ETFs, as we

discuss below.

A compelling alternative to money markets, CDs, and bond funds

In the June 2026 Fed dot plot, the US Federal Reserve

projected the fed funds rate to fall toward 3% over the long term. Should this happen, popular money market funds such as Vanguard VMFXX

would see their yields fall to approximately 3.10% from the mid-3s today. In addition, since Vanguard VMFXX targets a net

asset value per share of $1.00, VMFXX cannot have capital appreciation.

Some CD rates may currently seem attractive;

however, CDs often pay their income at the end of their term (compared to corporate bonds, which pay interest

semi-annually), can come with onerous call provisions, and lack capital appreciation opportunities.

Mega bond funds such as Vanguard VBTLX are not fixed income investments. They do not

pay a fixed coupon and do not return an investor's principal at maturity, as they do not have a maturity

date. Bond funds such as VBTLX own thousands of bonds, which drives muted (and often low) returns and makes

investors unable to build a portfolio that fits their investment objectives. Further, since bond funds and ETFs do

not trade relative to a par value and lack underlying financial metrics, investors cannot assess whether a

bond fund investment represents a compelling value.

Owning individual bonds vs. bond funds is the lowest-cost way to invest in bonds, as investors do not pay recurring fees based on a percentage of what they invest. In addition, bond funds incur significant trading costs. Bond funds do not disclose the amount of these costs and exclude them from the "expense ratio" fund managers, such as Vanguard, trumpet. By taking actions to limit our market impact, we have enabled our subscribers to purchase bonds at competitive prices and to maximize their corporate bond returns.

Why Own Corporate Bonds Now

We strongly advocate investors build bond portfolios over time; however, as of this update, there are several factors making now a compelling time to invest in individual corporate bonds:

- Investors seeking the best individual corporate bonds to buy now can lock in high yields for the long term. In addition, since Bondsavvy's recommendations are highly selective, we can identify bonds that can increase in price and achieve total returns higher than a bond's purchase date yield to maturity.

- The 12-month dividend yield for iShares IVV S&P 500 ETF was 1.06% as of May 31, 2026, about one-sixth the average YTM of our most recent individual corporate bonds to buy now. Income investors can generate higher income with greater principal protection by owning individual corporate bonds vs. dividend stocks.

- Illusory money market 7-day yields, such as those for Vanguard VMFXX, have fallen about 1.8 points since September 2024, to 3.58% as of June 30, 2026. They could fall further toward 3% should the US Federal Reserve cut rates further per the June 2026 Fed dot plot.

- The S&P 500 has been trading near a 29x trailing price-to-earnings (P/E) ratio compared to approximately 19x ten years ago, according to Gurufocus.com. Historically, investing in stocks at high multiples has been negatively correlated with investor returns.

- Funds mimicking the S&P 500, such as the $889 billion iShares IVV ETF, are not as diversified as the name "S&P 500" implies. As of June 30, 2026, the top-10 holdings of iShares IVV accounted for 36.4% of the fund's market value. The top-25 holdings accounted for 51.1% of the fund's value.

- Income distributions for bond funds and ETFs vary monthly and do not enable investors to lock in long-term income, as can be done with individual corporate bonds.

- Since bond funds and ETFs do not trade relative to par value and lack underlying financial metrics, investors cannot assess whether bond funds or ETFs are trading at compelling values.

Choose My Plan

Watch Free Sample