We founded Bondsavvy in 2017 to make bond investing easy and

more profitable for individual investors.

While we have narrowed down the corporate bond universe from 11,000

available bonds to a list of 61 recommended corporate bonds for Bondsavvy

subscribers, we receive questions as to how subscribers should allocate

investments across our recommendations.

Since Bondsavvy does not provide individualized advice, we

cannot tell each subscriber how to allocate our bond recommendations across an

entire investment portfolio. That said,

we can provide considerations and our ten "How To Build a Bond Portfolio" dos and don'ts

for Bondsavvy

subscribers to consider.

These include the following:

How to Build a Bond Portfolio: Ten Dos and Don'ts

- Do build your bond portfolio over time

- Do use bond price volatility to your advantage, when appropriate

- Do consider what's in your non-bond portfolio

- Do consider 'value' available in the marketplace when deciding how much to invest at a given time

- Don't build bond ladders

- Do diversify across industry groups

- Do invest in investment grade and high yield corporate bonds

- Do diversify across maturity dates

- Don't feel compelled to purchase bonds in large quantities

- Don't think cash and corporate bonds have the same level of security

Fixed Income Blog Post Overview

This fixed income blog post addresses “How to Build a Bond

Portfolio” and is primarily geared toward Bondsavvy subscribers who have access

to our corporate bond recommendations. Since Bondsavvy only recommends individual corporate bonds, these investments will be the focus of this article. Please read our corporate bonds advantages and disadvantages blog

post, which can help you decide whether you should

consider adding a greater exposure to corporate bonds in your investment

portfolio.

Since this fixed income blog post is geared toward Bondsavvy

subscribers, it does not start from square one on how to select compelling corporate

bond investments. Please read our corporate bond research blog post to learn the

factors we evaluate before

recommending bonds to Bondsavvy subscribers.

This Article's Recommendations Are Not Individualized Advice

Readers of this fixed income blog post will come from all

walks of life. They will have different

investment objectives, incomes, amounts to invest, time horizons, etc. Given this, the recommendations herein

are

not individualized advice but rather represent what we believe to be sound

practices when building a corporate bond investment portfolio.

We founded Bondsavvy to empower the individual investor. We provide a significant amount of

information regarding our bond recommendations and our approach to bond

investing. In the end, however, it is

the Bondsavvy subscriber who makes the final call on what bonds go into his or her investment portfolios.

How Many Bonds Should I Own?

A popular question posed by Bondsavvy subscribers is “How

many different bonds should I own?” As we discuss

in this fixed income blog post, we do recommend new bond investors start small

and build their portfolios over time. A

new bond investor could begin with investments across several different bonds

and build the portfolio over time. This section considers what a fully built-out bond portfolio could look

like.

No magic number of bonds

As of February 18, 2026, Bondsavvy recommended 61 individual

corporate bond CUSIPs as buy or hold. Since investors will have different holdings in their

non-bond portfolios, different risk profiles, and different corporate bond

holdings, there is not a “perfect” number of BondSavvy recommendations to

own. That said, we can provide general considerations as to the number of Bondsavvy recommendations subscribers

could hold based on certain factors.

Figure 1 is not meant to be prescriptive and is not individualized advice. Rather, it seeks

to provide a range of the quantities of bond CUSIPs subscribers may choose to own based on the risk of the corporate

bond and non-bond holdings. There are many caveats to this, including the importance of following the "How To

Build a Bond Portfolio" dos and don'ts discussed in this fixed income blog post.

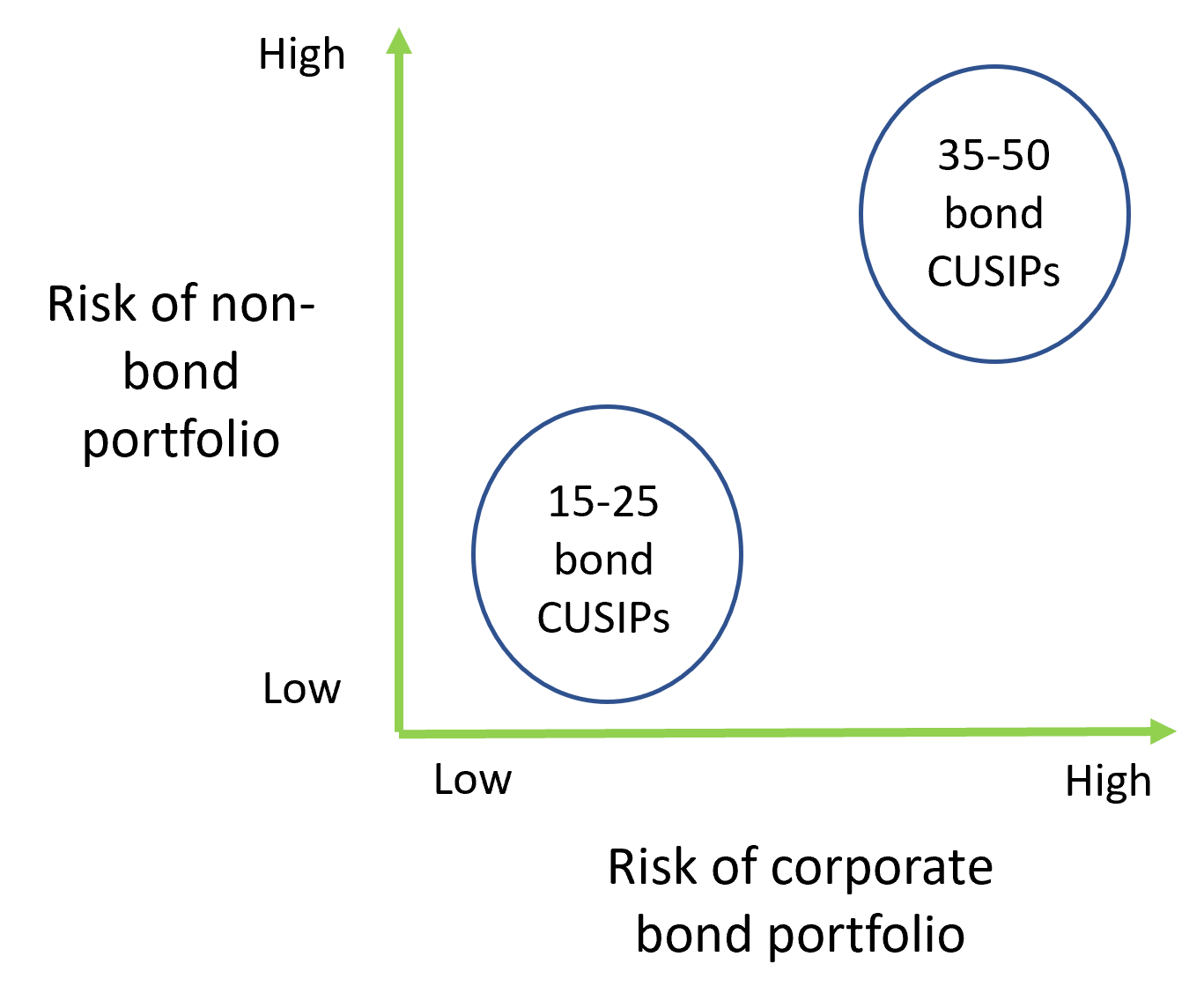

Figure 1: Potential Number of Bond Holdings Based on Portfolio Risk

Figure 1's underlying premise is that investors with higher-risk portfolios should consider owning

a wider variety of bonds. We recommend investors who have higher-risk non-bond portfolios and

higher-risk corporate bond portfolios own between 35-50 different corporate bond CUSIPs. Those with

lower-risk portfolios could consider owning a smaller number of bond CUSIPs; however, this will depend on investors'

risk tolerance and investment objectives.

Example of Low-Risk Non-Bond Portfolio

Investors with 'low-risk non-bond portfolios' would likely have a significant amount held in

cash, CDs, money markets, and other low-risk investments. These investors are generally risk averse. Such an investor may not need to own more than 15-25

Bondsavvy recommendations provided she was investing in our lower-risk recommendations. Owning a lower number

of recommended bonds can increase portfolio volatility; however, it can also help drive higher long-term

performance assuming no investments incur permanent capital loss.

Own Different Types of Bonds

In Figure 1, we provide general guidelines on the number of Bondsavvy recommendations subscribers

may choose to own based on certain factors such as the risk level of their corporate bond and non-bond

holdings. It's important to keep in mind, however, that accomplishing diversification in corporate bonds is

not just a question of owning a certain quantity of bonds. Rather, we believe investors should consider owning

a variety of bonds as they build their portfolios.

For example, since investment grade corporate bonds can be highly sensitive to US Treasury yields,

a portfolio with 30 corporate bonds that were all investment grade would not necessarily be a well-diversified

portfolio. As we saw in 2022, investment grade corporate bonds -- both long- and short-dated -- had some of

the worst bond performance due to their sensitivity to US Treasury yields.

As we discuss later in this fixed income blog post, we believe it's important for Bondsavvy

subscribers to own both investment grade and high yield corporate bonds since their price movements can be driven by different factors. Please read our corporate bond credit spreads blog post for a more

comprehensive discussion on key drivers of investment grade and high yield corporate bond prices.

Must Still Follow the Other Rules

The number of bond CUSIPs Bondsavvy subscribers may choose to own should not be considered in a

vacuum. Rather, investors must consider the quantity of bond CUSIPs they choose to own with the other

considerations discussed in this "How to Build a Bond Portfolio" article.

How To Build a Bond Portfolio: The Dos and Don'ts Explained

Recommendation 1: Do Build Your Bond Portfolio

over

Time

Many Bondsavvy subscribers are investing in individual

corporate bonds for the first time.

Building a bond portfolio over time is important for all investors, but

it is especially important for those new to bond investing.

It's okay to start small

Many investors will ask, “How much should I invest in bonds

to get started?” Some financial

advisors will respond to this

question with a gargantuan sum.

Do NOT listen to these folks.

We believe new bond investors should start small, as individual

corporate bonds are new territory for many investors. Investing mistakes can happen, and such

mistakes can be more common for new investors.

It's better for these mistakes to be made with a small-to-start amount

invested.

A key advantage to owning individual bonds vs. bond funds is

that, over time, individual bond investors should learn and improve. They will learn how and why different

bonds

can react to different market conditions.

They will learn from bond investments that performed well and others that did

not. They will better understand how to

use online brokerages such as Fidelity.com, E*TRADE, Schwab.com and others.

It is with this knowledge that investors could, potentially,

increase their exposure to individual corporate bonds over time.

Bondsavvy founder and fixed income expert Steve Shaw's first

investment in corporate bonds was one CUSIP where he purchased a quantity of

five bonds. As he had success investing

in corporate bonds, he increased his exposure to individual corporate bonds

until the point where it represented his entire investment portfolio.

Limit the risk of going 'all-in' at a bad time

The year 2021 was generally a good year for bond

investing. US Treasury yields did rise

slightly; however, bond defaults were minimal, and many bonds performed well.

While this seemed like a good time to invest, given 2022 was

one of the worst years in the history of the bond market, those who invested

heavily in 2021 would have likely seen their portfolios take a big hit in 2022. In addition, investors who

were 'fully

invested' in 2021 likely had limited resources available to take advantage of

bond prices that fell in 2022.

Figure 2: Bondsavvy Recommends Bond Investors NOT Go All-in at a Specific Time

Rome wasn't built in a day, and we believe successful bond

portfolios should be built over time, in part, to limit risk.

Take advantage of new opportunities as they arise

Bondsavvy makes new corporate bond recommendations each

quarter after companies report quarterly earnings. We do this during The Bondcast, an

interactive webcast series where fixed income expert Steve Shaw reviews

the investment rationale and financial analysis for each bond recommendation. We also update each bond

recommendation every

quarter with new buy/sell/hold ratings during The Super Bondcast.

We originally published this fixed income blog post in

February 2023. This followed one of the

worst years in the bond market of all time.

During 2022, the US Federal Reserve increased the target range of the fed funds rate

from 0.00% to 0.25% to 4.25% to 4.50%.

For most of the year, US Treasury yields, which have can have a big

impact on certain corporate bonds, increased. Later in this article, we will show examples of how different

corporate bonds behaved differently in the wake of high inflation and a hawkish US Federal Reserve.

While 2022 was one to forget for many bond investors, those

who left some money on the sidelines were able to purchase many corporate bonds

at all-time lows. These included long-term bonds

of some of the world's most profitable companies that, at the publication of

this fixed income blog post, were trading around 60 cents on the dollar. While these bonds may not return to

par in

the next 12-18 months, if they return to par over, say, five to ten years, this will

represent an outstanding return given the very low risk of default of

investment grade corporate bonds

Recommendation 2: Do Use Bond Price Volatility to

Your Advantage, When Appropriate

One of the key advantages of corporate

bonds vs. stocks and bond funds is that, so long as a bond issuer

doesn't go belly up, corporate bond prices are required to return to par value at maturity. Bond funds and stocks don't trade relative to par value and

neither provide a guarantee to return to any price in the future.

Individual bondholders can use this to their advantage to navigate bond price

volatility. Some of the most volatile bonds in the marketplace are long-term investment grade corporate

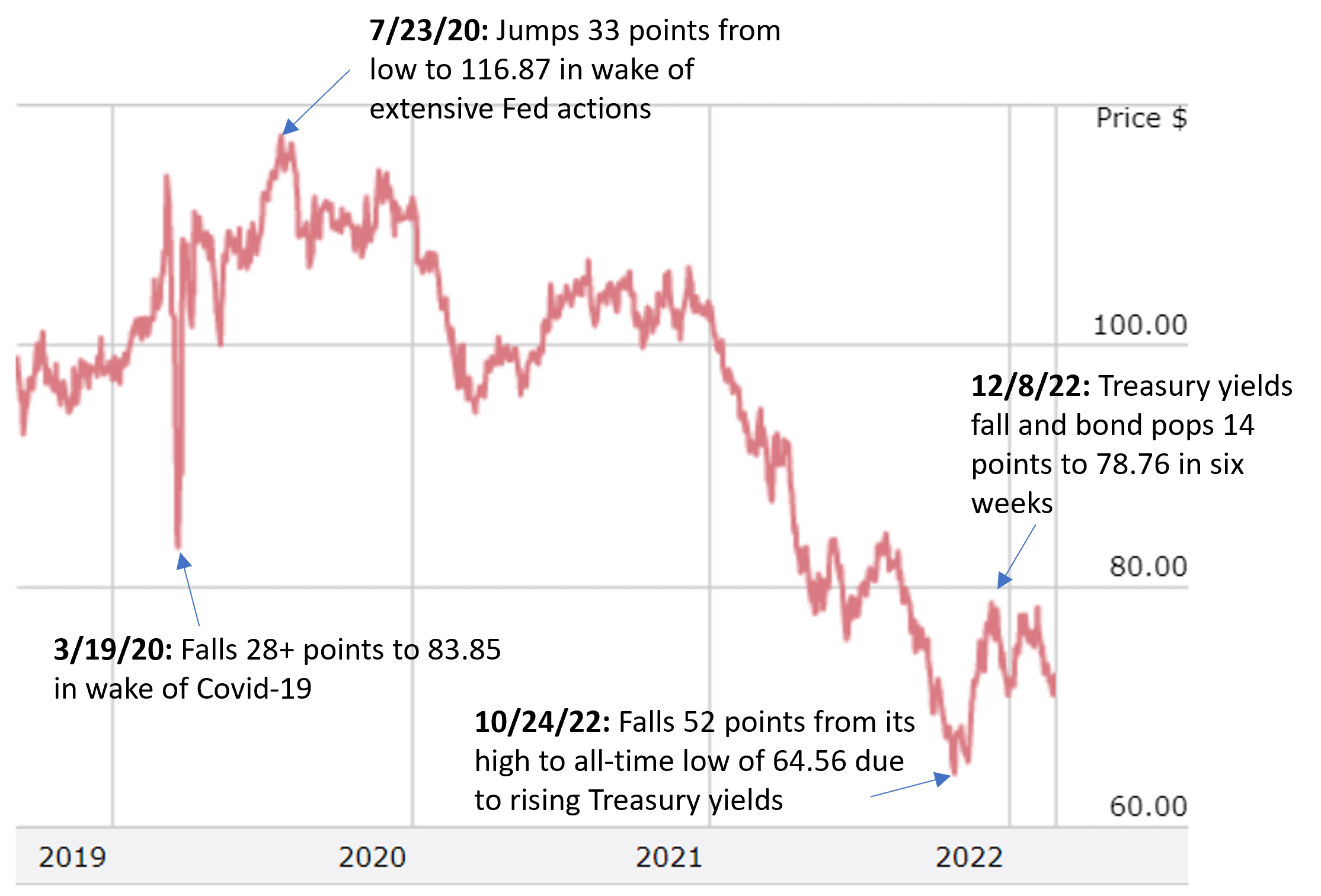

bonds such as the Apple 2.95% '49 bond (CUSIP 037833DQ0). Figure 3 shows the price action of this Apple

bond from September 4, 2019 until February 24, 2023. As discussed in our credit spreads

blog post, investment grade corporate bonds can be highly sensitive to movements in US Treasury yields.

This is especially true for long-dated investment grade corporate bonds such as the Apple '49 bond.

As shown in Figure 3, this Apple bond fell 52 points from its peak on July 23, 2020

to its low on October 24, 2022. Since Apple has a close to zero risk of default, investors can purchase

these bonds at a deep discount to par value, collect their coupons, and wait for the Apple bond price to

recover. While we do not have a crystal ball as to when these bonds may return to par value, it's likely

they will do so well before the 2049 maturity date.

Figure 3: Performance of Apple 2.95% 9/11/49 Bond -- Sep

4, 2019-Feb 24, 2023

Source: FINRA market data

Of course, different corporate bonds pose different levels of risk, and there are

bonds that can fall in price and have significant risk of never returning back to par value. It can,

therefore, often be a better risk-reward opportunity to take advantage of volatility in bonds of higher credit

quality (like an Apple bond or similar), as permanent capital loss is generally not in the cards for such

bonds.

Investors can take advantage of price volatility in high yield bonds; however, more

diligence is needed. Sometimes, a bond price can fall 30+ points due to a corporate bond rating

downgrade. These can, at times, be opportunities resulting from a trigger-happy ratings analyst; however,

they do often pose a higher degree of risk than capitalizing on volatility by bonds issued by companies such as

Apple.

Recommendation 3: Do

Consider What's in Your Non-Bond

Portfolio

An important factor impacting the recommendations Bondsavvy subscribers own is what other

investments are in the rest of their portfolios. This is one of the many reasons Bondsavvy cannot be

prescriptive about which of our recommended bonds subscribers should own, as non-bond portfolios will vary, as will

investors' risk tolerance and investment objectives.

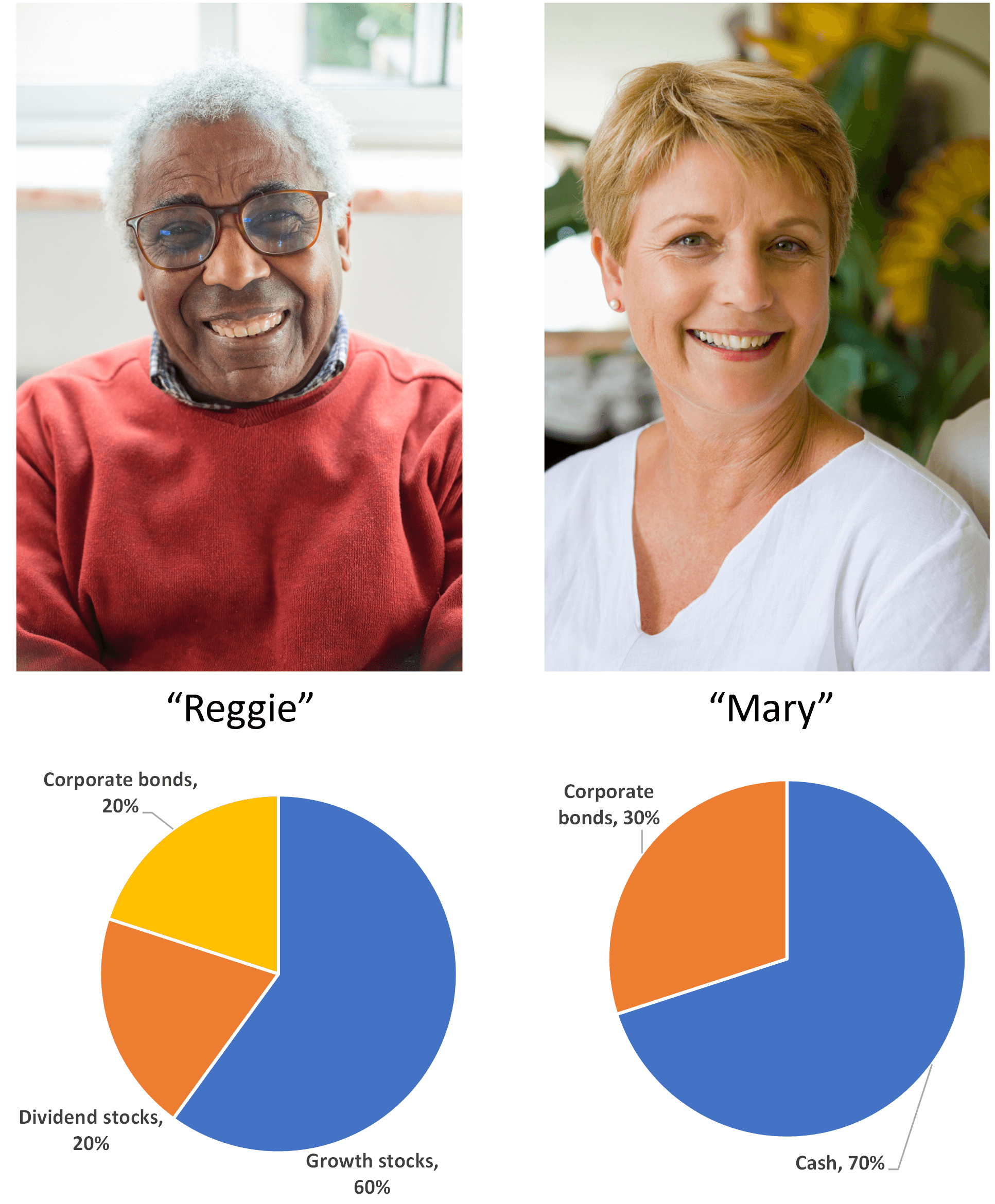

The case of two hypothetical investors, Reggie and Mary, illustrates our point:

Figure 4: Asset Allocation of Two Hypothetical Corporate Bond Investors

Both Reggie and Mary are regular visitors to Bondsavvy's leading bond investing website. They both

recently decided to invest in individual corporate bonds to take advantage of their strong potential returns,

income, and safety relative to stocks. As shown in Figure 4 above, Mary is a more conservative investor than

Reggie, as 70% of her portfolio is held in cash. Since Mary holds such a large portion of her non-bond

portfolio in cash, she may, at some point, choose to be more aggressive with her corporate bond portfolio than

Reggie, who already has a healthy portion of his portfolio in higher risk investments.

That said, Mary will need to make the final call as to whether she is ready to accept the

volatility -- and potential loss of capital -- associated with higher-risk corporate bonds.

What industries are in your non-bond portfolio?

Bondsavvy recommendations typically include bonds issued

by companies in about 15 different industry groups.

These industry groups have included: manufacturing, defense, travel, natural

resources, agriculture, healthcare, homebuilding, technology,

chemicals, automotive, transportation, media, retail,

communications, pharmaceuticals, and infrastructure. Many of these industry groups are broad, and

they could be further broken down.

In the case of our example in Figure 4, Reggie already owns growth and dividend stocks. Prior

to investing in Bondsavvy's recommendations, he should evaluate the industry concentration in his stock portfolio to

ensure Bondsavvy recommendations he buys do not overconcentrate his overall portfolio in a specific industry.

We further discuss the importance of industry diversification later in Recommendation 6 of this

fixed income blog post.

Recommendation 4: Do consider 'value'

available in the

marketplace when deciding how much to invest

Corporate bond investors can evaluate several metrics to

determine whether bonds available represent a good value. These include bond yields to maturity

(YTM), price relative to par value, and credit spreads. Since these metrics do not consider issuing company

financials, they are meant to provide an initial assessment of value. After evaluating these factors, we can

dig into

issuing company financials.

In Recommendation 7, we show historical bond price charts for three oil & gas companies.

These charts show how the three bond prices previously moved as a percentage of par value.

In this Section 4, we will focus on how investors can use movements in bond YTMs and in credit

spreads to assess a corporate bond's value. This will just provide a pre-financial-analysis view of value in

the market. Prior to making new bond recommendations, Bondsavvy completes its fixed

income investment analysis to determine whether a bond is a good value and whether it becomes a new

recommended bond.

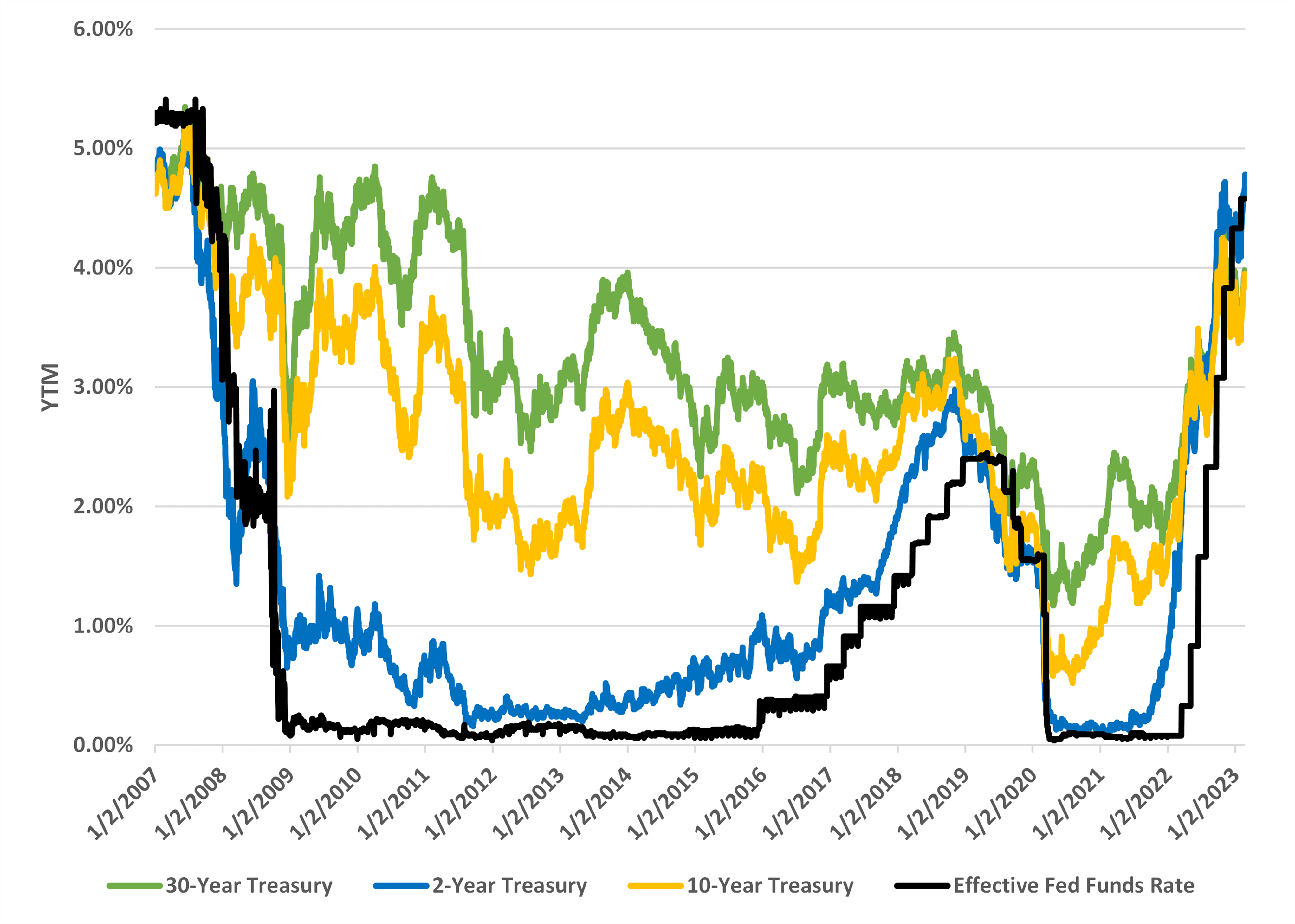

Assessing Value Based on US Treasury YTMs

Since corporate bonds, especially investment grade corporate bonds, can be heavily impacted by US

Treasury yields, investors must evaluate the level of US Treasury YTMs when making new investments. Figure 5

shows historical YTMs for the two, ten, and thirty-year US Treasurys. It also shows the effective federal

funds rate.

As shown, 10- and 30-year US Treasury yields had been trending down from 2008 until 2021 before

shooting up in 2022, as the US Federal Reserve aggressively raised the fed funds target rate. US Treasury

yields are volatile and up or down movements can switch quickly.

When most bond yields were super low in 2020 and 2021, finding value in corporate bonds was

difficult. In late 2022 and early 2023, with certain Treasury yields at heights not seen since 2007 and 2008,

there was a greater amount of value available in the market. The reason for this is that, with US Treasury

yields at these higher levels, there's an opportunity for these yields to fall and for certain bond prices,

including corporate bonds, to rise.

Figure 5: Historical US Treasury YTMs and Effective Fed Funds Rate -- Jan 2, 2007-Feb 24, 2023

Sources: US Treasury Department and Federal Reserve Bank of New York.

When deciding how aggressively to make new corporate bond investments, it's important for investors to assess where

we are with respect to historical US Treasury yields.

Assessing Value Based on Corporate Bond Credit Spreads

When purchasing a new corporate bond on Fidelity.com, investors can see the corporate bond's credit spread, or the

difference in yield between the corporate bond and the US Treasury that has a similar maturity date. The

credit spread represents the extra compensation, or yield, investors receive for taking on credit risk that is

deemed higher than that of the US Treasury.

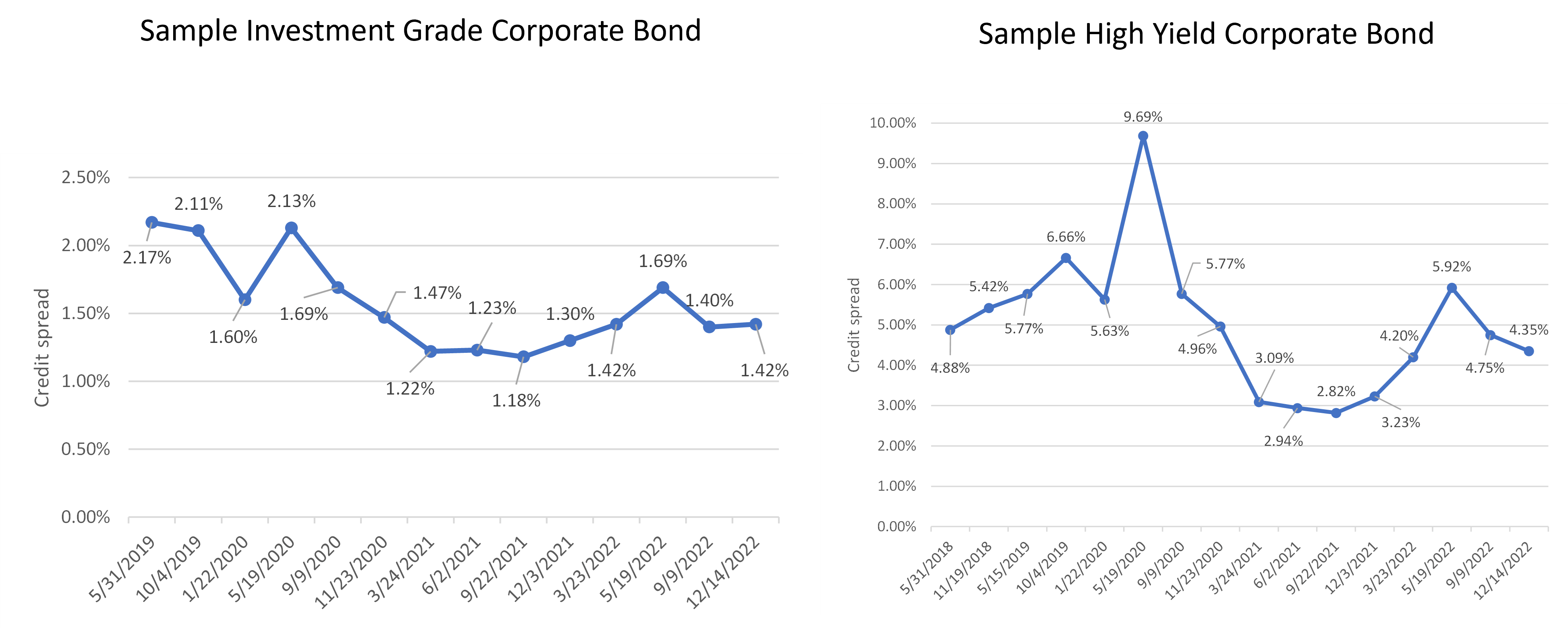

Figure 6 shows the historical credit spreads for two BondSavvy-recommended bonds: one rated

investment grade and the other a high yield corporate bond. It shows the credit spreads beginning the date we

made the initial recommendation and then on each date we updated the recommendation during The Super

Bondcast.

When we initially recommended the investment grade bond on May 31, 2019, it had a credit spread of

2.17%, which has been the high water mark of the bond's credit spread since the pick date. On December 14,

2022, the bond had a credit spread of 1.42%. Since this credit spread is materially lower than the pick date

credit spread, this bond had less credit-spread-related "upside" on December 14, 2022 than it did on the pick

date. When we say "credit-spread-related upside," we mean a credit spread's ability to fall, which could drive

a corporate bond's YTM lower and the bond's price higher.

Figure 6: Historical Credit Spreads for Two Bonds -- Pick Date to December 14, 2022

Source: Credit spreads from Fidelity.com. Charts created by BondSavvy

The range of credit spreads for the high yield bond is much wider than that of the investment grade

bond. While the high yield bond's credit spread on December 14, 2022 (4.35%) was only slightly lower than the

pick date credit spread of 4.88%, it went as high as 9.69% in mid-2020 in the wake of the Covid-19 crisis. One

of our mistakes was not selling this bond when its credit spread had fallen to below 3.00%, as it's not clear if and

when this bond's credit spread can return to such levels.

As noted above, evaluating US Treasury YTMs and corporate bond credit spreads is only the first

part of identifying value. When determining which bonds make our recommended list, we compare these bond

pricing metrics to issuing company

financial metrics such as leverage ratios, interest coverage ratios,

profitability growth, and all of the factors we consider in our corporate

bond research.

Recommendation 5: Don't Build Bond Ladders

We have written a separate blog post on “Why Bond Ladders Are Broken.” For the reasons we discuss

in that blog post, we believe an active approach focused on identifying bonds

with compelling values can drive higher total returns than bond ladder strategies. A big part of our fixed income

investing strategy is to sell bonds before maturity to lock in capital gains and maximize total

returns. As we summarize below, we

believe bond ladder strategies limit returns

and increase risk.

When BondSavvy recommends a new bond, we conduct comprehensive

corporate

bond research to assess a bond's risk and potential upside. This investment analysis identifies bonds

that can increase in price and achieve corporate bond returns that beat the leading bond funds and ETFs.

The initial recommendation is only when the work begins, as we then update each buy/sell/hold recommendation every

quarter based on the issuing company's financial performance and the price performance of each recommended bond.

We believe corporate bond ladders limit investment returns and increase risk due to the following

reasons:

- Bond ladders use a bond's maturity date as the primary

investment criterion

- Since bond ladders hold bonds to maturity, the highest return an investment can achieve is a bond's YTM on the

purchase date. Investors don't generally buy low and sell high with bond ladders

- At the creation of a bond ladder, there is a large initial investment of capital, which attempts to time the

market. This violates Recommendation 1 of How To Build a Bond Portfolio

- Bond ladders seek to return principal on a specific date rather than attempting to maximize performance over the

long term

- Bond laddering is a 'set it and forget it' strategy that lacks the rigor of our active investment

approach. Since the financial performance of the issuing companies is not regularly evaluated, we believe

bond ladder default risk is higher than that of an active bond investing approach

As bond yields rose in 2022, we began recommending short term investment grade corporate bonds, as their

yields finally reached compelling levels. We may decide to hold some of these bonds to maturity, as we

selected these bonds to lock in returns over two- to four-year periods. Holding bonds to maturity can make

sense in certain cases; however, we believe maintaining holding period flexibility is a big factor in maximizing

investment returns over the long term.

Recommendation 6: Do Diversify Across Industry Groups

On February 22, 2023, BondSavvy's 52 corporate bond

recommendations covered companies across 16 industry groups. One of the many benefits of owning individual

bonds vs. bond funds is that investors can create a portfolio that suits their

investment objectives. They can also

tailor it to reflect expertise they may have across different companies and

industry groups.

We discuss later the importance of owning bonds with bond ratings of both investment grade and

high yield. We recommend this since, generally speaking, investment grade and high yield bond prices are

driven by different factors, and we don't want our bond portfolio to be a one-trick pony.

The same can be said for owning bonds in different industries. It is difficult to predict,

year in and year out, which industries can outperform over the next several quarters. While BondSavvy's fixed income

investment strategy does consider how a bond issuer's industry can perform when we make a recommendation,

corporate financial performance is often not a straight line.

Owning bonds issued by companies of different industries helps mitigate risk and can position

investors to capitalize when a specific industry does particularly well. For example, through the date of this

fixed income blog post, BondSavvy had recommended seven bonds issued by companies in the oil & gas

industry. We began making these recommendations as the economy began recovering in the second half of

2020. While we have sold several of these oil & gas bonds, the ones we held during 2022 generally held

their value and delivered positive returns in the wake of one of the worst bond markets in history.

Recommendation 7: Do Own Both Investment Grade and High Yield

Corporate Bonds

While we are not big believers in corporate bond ratings,

investors must understand how bond ratings can impact the trading activity of

corporate bonds. Corporate bonds are not

a monolithic asset class, and different bonds will behave in different ways.

For example, investment grade corporate bonds, especially

those with a longer time to maturity, can be heavily impacted by changes in US Treasury

yields. High yield corporate bonds, on

the other hand, are impacted, to a greater extent, by the financial performance -

and perceived creditworthiness - of the issuing company.

We encourage BondSavvy subscribers to own both investment

grade and high yield bonds because we don't want all of our bond holdings to

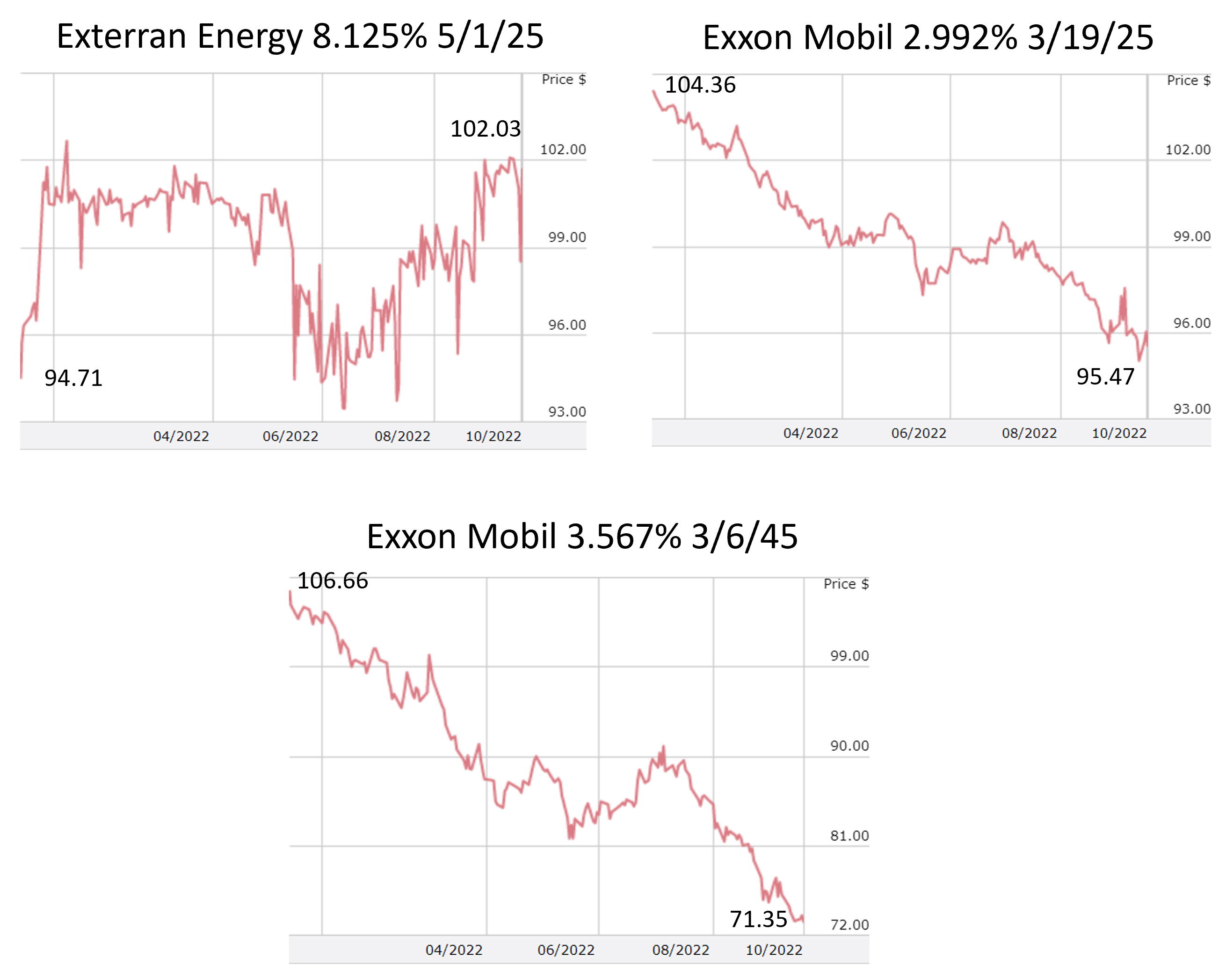

behave in a similar way. We illustrate this point in Figure 7 by showing the bond price performance of three

bonds issued by oil & gas companies.

On January 12, 2022, we recommended BondSavvy subscribers purchase the Exterran Energy 8.125%

5/1/25 bond (CUSIP 30227KAE9) at a price of 94.71. Exterran was a natural gas processing and treatment

("midstream") provider based in Houston, TX. At the time of the recommendation, the Exterran bonds were rated

B3 / B by Moody's and S&P, had a YTM of 10.08% and a credit spread of 8.83% (or 883 basis

points).

Shortly after our recommendation, Canada-based Enerflex announced its acquisition of

Exterran. Since Enerflex had a higher bond rating than Exterran and the Exterran bonds would be assumed as

part of the transaction, the Exterran bonds traded up. Later, on October 21, 2022, the Exterran bonds were

called at a price of 102.03, which generated an investment return of 14.36% vs. a -13.51% return for the iShares HYG

high yield corporate bond ETF.

Figure 7: Corporate Bond Prices of Exterran Energy vs. Exxon Mobil Bonds -- January 12,

2022-October 21, 2022

Source: FINRA market data.

As shown in Figure 7, both the Exxon Mobil '25 (CUSIP 30231GBH4) and Exxon Mobil '45 (CUSIP

30231GAN2) bonds performed poorly during the holding period of the Exterran bond, with the Exxon Mobil '25 bond

falling nine points and the Exxon Mobil '45 bond falling 35 points. In the case of Exxon Mobil bond investors,

they picked the right industry for 2022; however, since these bonds are rated investment grade (Aa2/AA-) and highly

sensitive to US Treasurys, 2022 was a year to forget.

Of course, not all years will be as bad as 2022 for bond investors. Moreover, investors in

2022 and early 2023 were able to purchase bonds issued by the world's most profitable companies at significant

discounts to par value.

Please read our corporate bond credit spreads blog post for a detailed discussion on what

causes corporate bond prices

to move and how this varies between investment grade and high yield corporate

bonds.

Recommendation 8: Do Diversify Across Maturity Dates

Investment grade corporate bonds are typically issued with maturity dates of 20 to 40 years compared to 5 to 10 years

for high yield corporate bonds. Owning a variety of both investment grade and high yield bonds will

take investors part of the way -- but not all the way -- to diversifying across maturity dates.

The number of bonds issued by companies can vary. Some companies may have over 100 bonds outstanding while

others may have fewer than a handful. Since high yield bond issuers are often smaller in size than investment

grade issuers, some high yield bond issuers may only have two or three bonds from which to select. As part of

our fixed income research, we then evaluate the trading activity of each bond and whether it has sufficient bid-ask

quotes to satisfy increases in trading volume driven from a new BondSavvy recommendation.

This is a circuitous way of saying that a high yield bond investor may not necessarily be able to

choose from a wide variety of maturity dates of a given high yield bond issuer.

As noted in this fixed income blog post, in 2022, BondSavvy began recommending short term corporate

bonds due to the compelling yields they were offering. This augmented our prior recommendations of long-dated

investment grade corporate bonds. Given how poorly long-dated investment grade corporate bonds performed

during 2022, we wanted to have a portion of short term bonds where we could count on a mid-single-digit return over

the next several years.

Such short term bond opportunities had not presented themselves until 2022. Given that we

don't want all the bonds in a corporate bond portfolio to behave in a similar way, it's important for investors to

take advantage of maturity-diversification opportunities when they can.

A note on Fallen Angel bonds

A bond is said to be a "Fallen Angel" when its corporate bond rating is downgraded from investment

grade to below investment grade. Since Fallen Angels were initially issued with an investment grade rating,

such bonds generally have certain characteristics of investment grade bonds such as longer maturity dates. It

is, therefore, often more possible for investors to find a wider variety of maturity dates with Fallen Angels than

it is with bonds rated below investment grade on the date of issuance.

Recommendation 9: Don't Feel Compelled to Buy Bonds in Large

Quantities

Your last name does not have to be Rockefeller to invest in individual corporate bonds. By investing in bonds

online, individual investors can transact in bond trade sizes as few as two bonds, or $2,000 in par value of bonds. Since investors can purchase

bonds in smaller quantities, they can build positions over time rather than feeling compelled to purchase a large

quantity in one transaction.

Companies such as Fidelity, E*TRADE, Charles Schwab,

Interactive Brokers, Tradeweb, Intercontinental Exchange, and others have

made investing in individual corporate bonds fair for investors. These companies have built online trading

platforms that aggregate corporate bond bid-ask quotes that retail brokerages display to their individual investor

clients. Investors can click on live bond quotes and execute trades within seconds.

While quoting levels can vary by bond and be impacted by market conditions, individual corporate

bonds often have at least six bid and offer quotes. This level of competition drives narrow bid-ask spreads

and high-quality trade execution for individual investors.

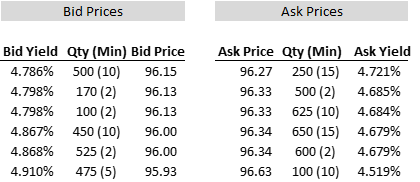

Figure 8 shows the depth of book for the Microsoft 2.700% 2/12/25 bond (CUSIP 594918BB9). The

"depth of book" shows both bid and ask quotes provided by dealers to facilitate corporate bond trading

activity. We discuss key takeaways from this table below Figure 8.

Figure 8: Depth of Book for Microsoft 2.70% '25 Bond on February 24, 2023

Takeaway 1 -- Minimum quantities of 2 to 15 bonds

The minimum quantity associated with each bid or ask quote is the number in parentheses in Figure

8. While they can vary slightly, minimum quantities typically available when investing in

corporate bonds online are 2 to 10 bonds. For the Microsoft 2.70% '25 bond, however, minimum

quantities were 2 to 15 bonds on February 24, 2023.

On the ask side (the price at which investors purchase bonds), the minimum quantity for the

"top-of-book" (or best) price of 96.27 was 15 bonds. For investors seeking to purchase a quantity of 2 to 14

bonds, they would need to execute at the slightly worse ask price of 96.33, a price that had a minimum quantity of

two bonds.

While it can be helpful to own corporate bonds in larger quantities, it may or may not affect the

price at which you execute your trade. As shown under the bid prices in Figure 8, an investor looking to sell

five bonds -- rather than 10 -- could have sold the bonds at 96.13, a smidge lower than the 96.15 top-of-book bid

price.

Since investing in bonds over time is central to our approach on "How To Build a Bond Portfolio,"

investors can build a position over time to limit timing risk or to take advantage of bond prices that

have fallen. For example, investors who had trepidation about the Federal Reserve raising interest rates in

2022, could have built a 25-bond position in this Microsoft bond over time rather than buying all 25 bonds at once.

Takeaway 2 -- Narrow bid-ask spread

Many investors are surprised as to how competitive corporate bond quotes are for individual

investors. As shown in Figure 8, the bid-ask spread for this Microsoft bond was 0.12 points (the difference

between the 96.15 and 96.27 top-of-book bid-ask quotes). On a YTM basis, the bid-ask spread was 6.5 basis

points (or 0.065 percentage points). When buying bonds online at brokerages such as Fidelity.com and E*TRADE,

bond investors can compare these live quotes to corporate bond trades reported to FINRA's TRACE reporting system.

The notion that individual investors "get ripped off" when trading individual bonds is far from the

case. While bid-ask spreads and the number of live quotes can vary, individual investors generally benefit

from robust levels of bond quotes and easy-to-use online brokerages that offer fast and efficient trade execution.

Recommendation 10: Do acknowledge that corporate bonds are not cash investments

Since company bonds are senior to a company's common stock, some investors treat corporate bonds as

if they are as good as cash. They are not. As shown in this fixed income blog post, corporate bond

prices can be volatile -- especially high yield corporate bonds and long-dated investment grade corporate

bonds.

There are some bonds, such as short-term bonds (1 to 3 years) of the highest-credit-quality issuers

that can be a good place to park cash; however, investors needing cash in one year should not invest

this amount in a three-year bond, even if it's a AAA-rated entity such as Microsoft.

With US Treasury yields rising during 2022, there were, finally, short term investment grade corporate bonds with

compelling yields. While this resulted in BondSavvy recommending such short term bonds for the first time,

investors must know that even these bond prices can fluctuate, albeit generally much less than high yield and

long-dated investment grade corporate bonds.

BondSavvy's Role in Building a Bond Portfolio

We founded BondSavvy to empower the individual investor. We didn't believe bond investors

were well served with opaque, underperforming bond funds. In addition, since corporate bond ratings don't

speak to whether a bond is a good investment, we felt bond investors deserved an independent analysis that

identified bonds that could outperform the leading bond funds and ETFs.

While many advancements have been made to make buying bonds

online efficient, before BondSavvy, individual investors still have to sift through 9,000 available

corporate bonds. BondSavvy changed this in September 2017, when it presented its first set of corporate bond

recommendations. Each quarter, we present between four to six new corporate bond recommendations during The

Bondcast, an exclusive webcast with subscriber Q&A. We then update all of our bond recommendations

each quarter based on our issuing companies' financial performance and the price performance of each bond.

Our goal is to make bond investing easy and more profitable for individual investors.

Click the "Get Started" button to learn about BondSavvy's subscription options or the "Watch Free

Sample" button to watch two free editions of The Bondcast. Let's get BondSavvy!

Get Started

Watch Free Sample