Using muni bond tax equivalent yields as the basis for a new bond investment is a big mistake. Since municipal bonds are typically callable long before maturity at par value, investors cannot rely on a municipal bond's coupon until maturity. In addition, with the onerous par call provisions, muni bond capital appreciation opportunities are limited, which further reduces their potential after-tax investment returns compared to corporate bonds.

This fixed income blog post discusses the reasons investors should not focus on muni bond tax equivalent yields when evaluating corporate bonds vs. municipal bonds. Key points include:

- Muni bonds have no promise of income until maturity. On average, twenty-year muni bonds are callable at par value 12 years before maturity**, placing investors' receipt of future coupon payments in doubt.

- Punitive par call provisions limit muni bond capital appreciation and after-tax total returns. If a muni bond is callable at par in several years, the bond isn't going much higher than par. On the other hand, investment grade corporate bonds have favorable call provisions that enable more capital appreciation and higher after-tax total returns.

- Muni bond tax equivalent yield calculations can overstate tax savings. For muni bonds trading at a discount to par value, capital appreciation between the purchase and maturity dates can be a significant part of a bond's yield to maturity. Since corporate and muni bondholders currently pay the same US capital gains tax rate, grossing up the capital gain portion of a municipal bond's YTM is inaccurate and overstates muni bond tax equivalent yields.

Since this analysis focuses on tax equivalent yields, we are assuming bonds are held in a taxable account. Of course, tax-deferred accounts, such as IRAs and 401(k)s, offer corporate bonds additional opportunities for higher total investment returns than municipal bonds.

Prevalence of Punitive Municipal Bond Call Provisions

If the coupon income from a municipal bond is not guaranteed until maturity, investors should not calculate a tax equivalent yield that assumes investors receive the bond's coupon until maturity.

Municipal bonds have performance-killing call provisions where bonds can be called, at par value, long before maturity. Investment grade corporate bonds, on the other hand, have make whole call provisions whereby bond issuers have to pay bondholders the present value of all future interest and principal payments to call the bond prior to maturity.

In Figure 1, we analyze a recent Fidelity bond search for municipal and corporate bonds. As shown, of the 18,419 municipal bonds maturing from August 2034 to August 2036, the median municipal bond was callable four years prior to maturity. Thirty-six percent (36%) of these municipal bonds were callable at least six years before maturity. For investment grade corporate bonds, the median bond was callable at par value three months before maturity.

Figure 1: Municipal Bond vs. Corporate Bond Call Provisions from Fidelity.com Bond Searches*

| # Bonds

in Sample | Median # Years

Callable @ Par

Before Maturity |

|---|

| August '34-August '36 Maturities | | |

| Municipal bonds | 18,419 | 4.00 |

| Corporate bonds | 711 | 0.25 |

| | |

| August '44-August '46 Maturities | | |

| Municipal bonds | 1,520 | 11.01 |

| Corporate Bonds | 382 | 0.50 |

*Bond searches made on August 21, 2025.

For municipal bonds maturing between August 2044 and August 2046, 92% were callable at par value at least 10 years before maturity, with the median bond callable 11 years before maturity. Suppose an investor owns a municipal bond, and the issuer calls the bond 10 years before maturity. If municipal bond yields fall, there is a good chance the bond will be called so the issuing entity can reduce interest expense.

In this case, the bondholder will have to replace the bond with another bond at a lower interest rate. Also, since the bond was callable at par value, capital appreciation driven by the decline in bond yields will be limited, as investors will not want to pay a price materially above par when the bond can soon be called at par.

Should bond yields rise and municipal bond prices fall, given how difficult and inefficient it is to sell municipal bonds (discussed later), replacing the bond with a higher-yielding bond would be difficult, especially when compared to how easy it is to sell corporate bonds before maturity.

We should note that this article focuses on municipal bonds vs. investment grade corporate bonds, as we wanted to compare bonds with similar creditworthiness. Call provisions for high yield corporate bonds are not as bondholder friendly as those for investment grade bonds, as such bonds will generally be callable -- at a premium to par value -- several years before maturity. These high yield bond call provisions are still generally more favorable than municipal bond call provisions. In addition, high yield bonds typically have lower interest rate risk and higher coupons than investment grade bonds.

Muni Bonds Have No Promise of Income Until Maturity

Municipal bonds' onerous call provisions make investors unable to count on munis for long-term interest income. Muni bond call and reinvestment risk is off the charts.

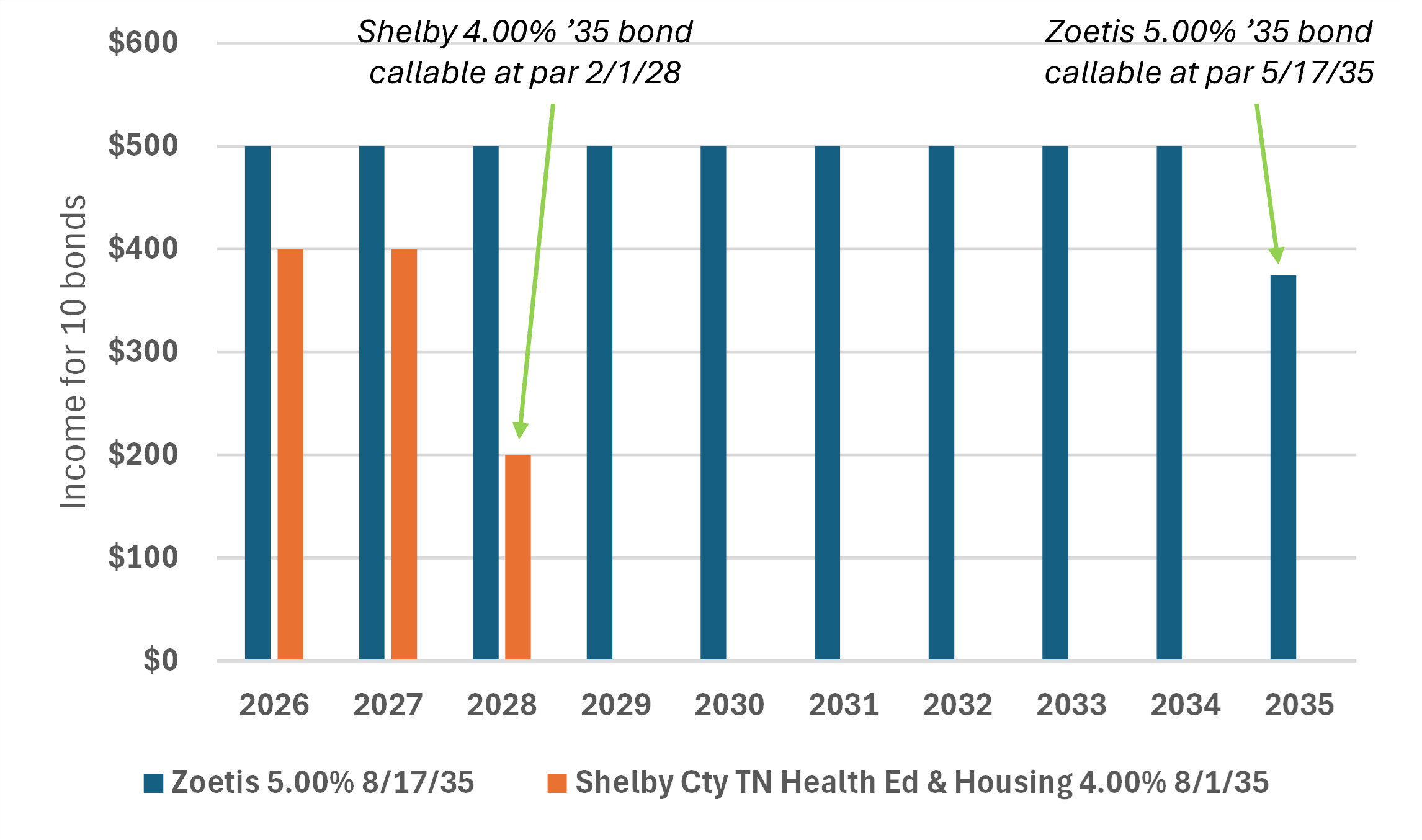

Figure 2 illustrates interest payments for a municipal bond and an investment grade corporate bond. The Shelby County, TN Health Educational & Housing 4.00% 8/1/35 bond (CUSIP 821697V30) is callable at par value beginning February 1, 2028. The corporate bond, Zoetis 5.00% 8/17/35 (CUSIP 98978VAX1), was issued by the animal pharmaceutical company and is callable at par value three months before the bond's August 17, 2035 maturity date.

Bondsavvy Subscriber Benefit

Steve Shaw founded Bondsavvy in 2017 to make bond investing easy and more profitable for individual investors. Our corporate bond recommendations cut through the clutter to identify bonds that

offer high coupons and upside potential relative to their risk.

Get Started

Figure 2 assumes a bondholder owns ten bonds and shows the income due to be paid each year up until the first par call date. The chart illustrates the stark difference between the two bonds' call provisions, as Shelby '35 bondholders can only count on bond coupon payments until February 1, 2028, 7.5 years before the bond's maturity date.

This creates significant reinvestment risk for the Shelby '35 bondholders, as, come February 1, 2028, there's no telling whether a 4.00% coupon for a similar muni bond will be available. Zoetis '35 bondholders do not have this risk.

Figure 2: Expected Interest Payments for Sample Municipal vs. Corporate Bonds up until First Par Call Date

Assumes 10 bonds owned

Later, we discuss how calculating a muni bond's tax equivalent yield based on the bond's YTM can overstate tax savings when the bond is priced at a discount to par value.

On August 21, 2025, the Shelby '35 and Zoetis '35 bonds had yields to worst of 3.89% and 4.99%, respectively. Both bonds were priced near par value: Shelby '35 at 100.26 and Zoetis '35 at 100.09.

Assuming a 24% federal income tax bracket and no state income taxes for Tennessee, the Shelby '35 tax equivalent yield would be 5.12%, slightly above the Zoetis bond's 4.99% yield to worst, a difference of 13 basis points. In this case, we believe the 13 basis-point higher yield for the Shelby '35 bond is outweighed by Zoetis '35's seven-plus years more of contractual interest payments and the greater capital appreciation opportunities corporate bonds can provide, as we discuss in the next section.

Corporate Bonds Have Greater Capital Appreciation Opportunities vs. Muni Bonds

Onerous call provisions create another muni bond investment disadvantage: limited capital appreciation opportunities relative to corporate bonds. In the Figure 2 example, since the Shelby '35 bond is callable at par beginning February 1, 2028, the bond price will be hard pressed to move more than negligibly above par value. On August 21, 2025, the bond's offer price on Fidelity.com was 100.26. If the Shelby '35 bond price moved to 102.00, its yield to worst would be a meager 3.16%. With 9.75 years until its first par call date, the Zoetis '35 bond has a greater upside opportunity, which could positively impact its total return.

Apart from more favorable call provisions, individual corporate bonds have two other advantages vs. municipal bonds when it comes to capital appreciation. First, key events, such as a mergers or strong earnings, can have a significant impact on a corporate bond's price. Second, since corporate bonds trade in a far-more-liquid market than muni bonds, they are easy to sell before maturity to lock in capital appreciation and maximize total returns.

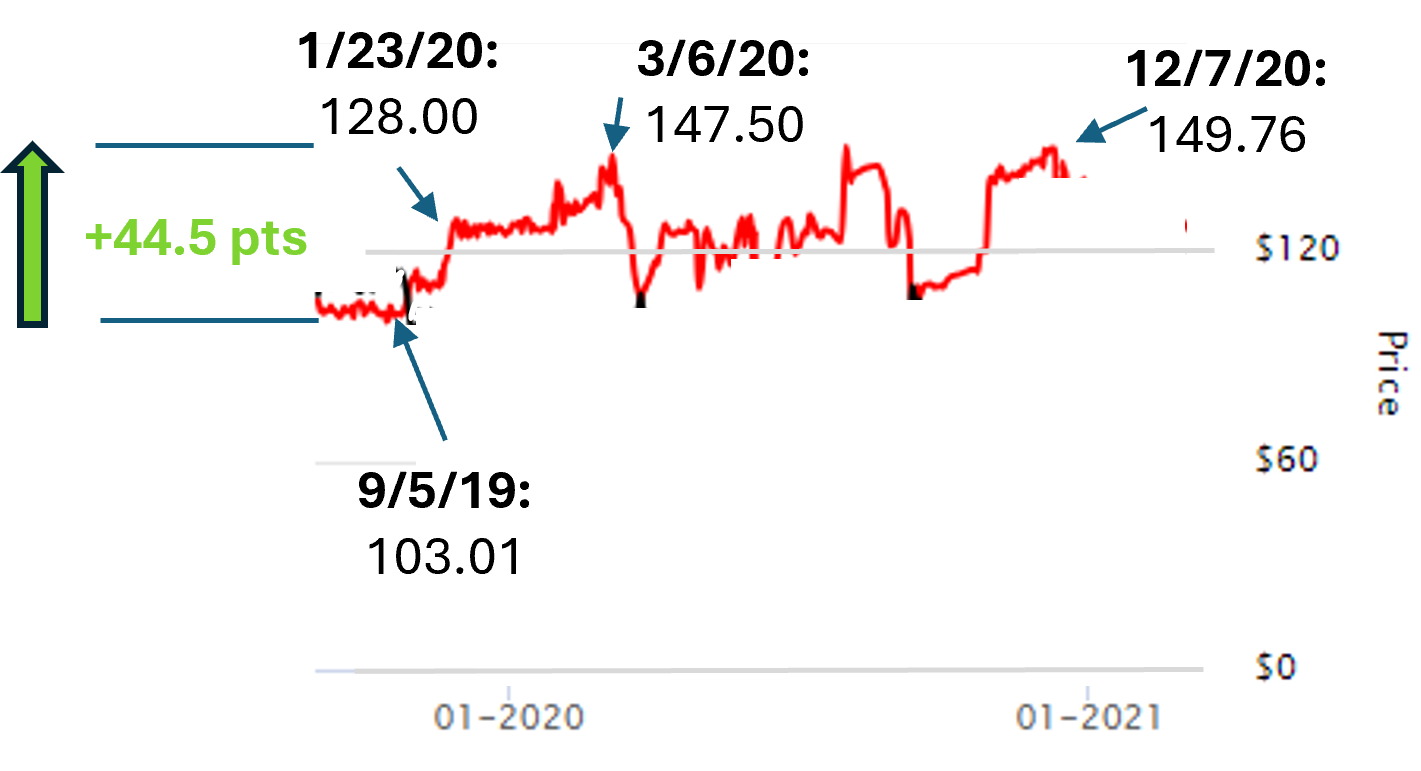

Figure 3 shows the historical prices of the Tiffany 4.90% '44 bond. As shown, the bond was trading at 103.01 on September 5, 2019. Then, on November 25, 2019, LVMH announced it was purchasing Tiffany. LVMH would assume the Tiffany bonds as part of the deal.

Since LVMH was larger and had a higher bond rating than Tiffany, the Tiffany '44 bond surged 25 points by January 23, 2020, closing at 128.00. Then, as US Treasury yields fell in the wake of Covid-19, the Tiffany '44 bond continued to rally, reaching nearly 150 by March 6, 2020.

Figure 3: Example of Corporate Bond Price Appreciation -- Tiffany 4.90% '44

Source: FINRA market data.

This level of potential price appreciation is unique to corporate bonds, as the credit quality of corporate bond issuers can change materially based on market events and financial performance. Since the Tiffany '44 bond was subject to a make whole call and not an early-dated par call like muni bonds, total capital appreciation in six months was nearly 45 points.

Of course, if we want to lock in capital appreciation in the case of the Tiffany '44 bond, we needed a liquid market to sell the bonds. Significantly higher trading activity and live bid-offer bond quotes enable individual investors to sell corporate bonds before maturity at good prices. Below in Figure 6, we show examples of municipal and corporate bonds, which illustrate how narrow corporate bond bid-ask spreads typically are.

Muni Bond Tax Equivalent Yields Can Overstate Tax Savings

Generally speaking, municipal bond interest payments are exempt from federal income taxes and, if you live in the state where the municipal bond was issued, state income taxes. Capital gains on both municipal and corporate bonds are subject to the same tax rate in the United States.

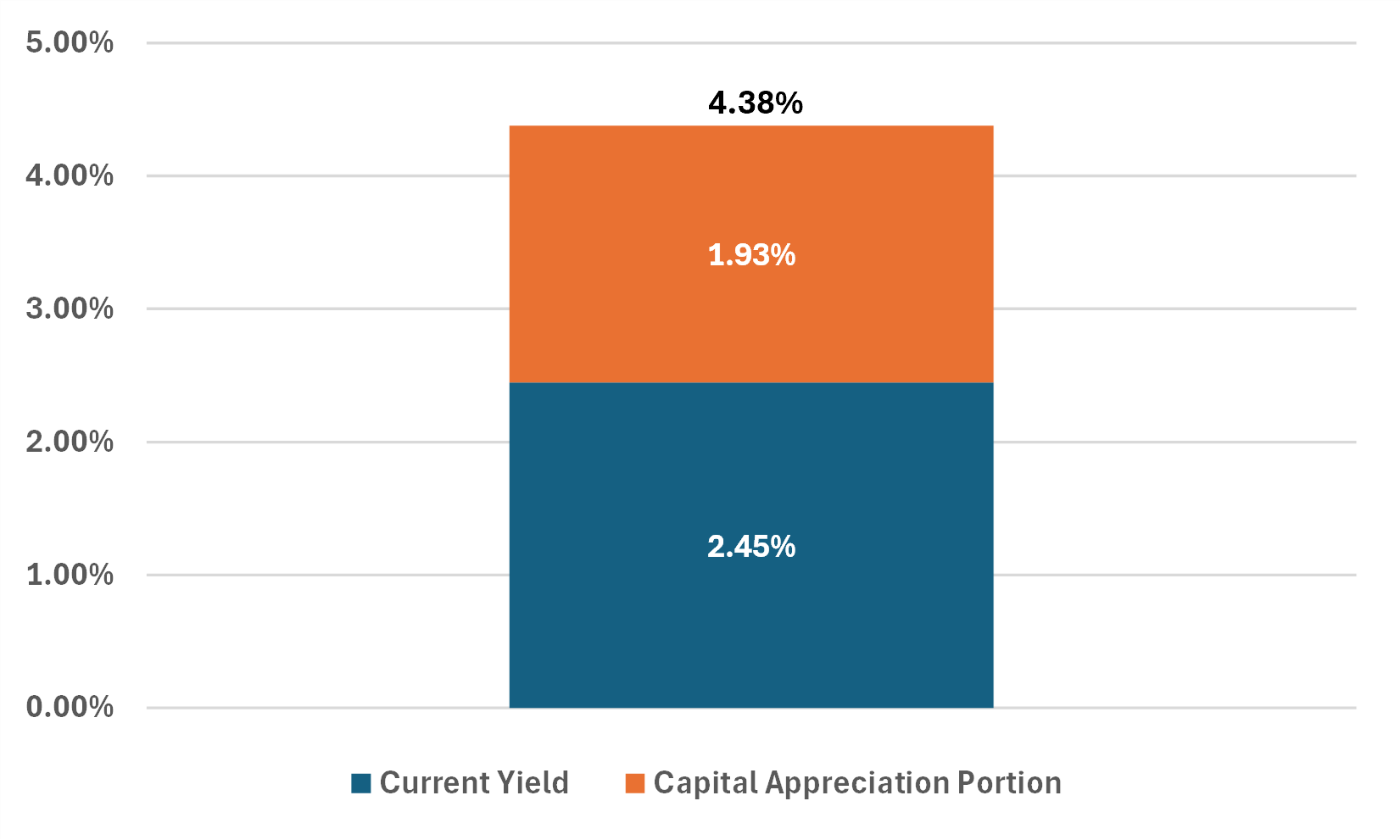

Depending on where a municipal bond is priced relative to par value, a significant portion of a municipal bond's yield to maturity can be the bond's expected capital appreciation between the purchase and maturity dates. Figure 4 shows the components of the Harris County, TX Department of Education 2.00% 2/15/35 (CUSIP 414015DA2) bond's yield to maturity. Since this bond had an offer price of 81.72% of par value on August 21, 2025, a significant portion of the bond's YTM was driven by expected capital appreciation between this date and the maturity date. In this case 1.93% of the bond's 4.38% YTM (about 44%) was from expected capital appreciation.

Since capital gains are taxed at the same rate for both muni and corporate bonds, calculating a municipal bond tax equivalent yield based on the muni bond's YTM overstates the tax equivalent yield. This is most relevant when a muni bond is priced at a discount to par value.

Figure 4: Components of Harris County, TX Dept Ed 2.00% '35 YTM -- Aug 21, 2025

Source: YTM from Fidelity.com. Current yield and capital appreciation portions calculated by Bondsavvy.

We calculated the bond's current yield by taking the $20 annual coupon and dividing it by the bond's market price of $817.20. The 2.45% current yield is the income portion of the 4.38% YTM, with the remainder driven by expected capital gain.

How Investors Are Currently Calculating Muni Bond Tax Equivalent Yields

Investors calculate a tax equivalent yield to determine the yield necessary for taxable investments, such as corporate bonds, to achieve the same after-tax returns of a municipal bond. Of course, this formula assumes that the municipal and taxable bond have similar other terms (such as call provisions), which they do not.

When we have scoured the Internet's muni bond tax equivalent yield calculators, the formular's numerator (per Figure 5) is "municipal bond yield." The calculators don't tell you if they're referring to a bond's YTM, yield to worst, or current yield; however, we believe most investors assume they are to use the municipal bond's yield to maturity.

We show the prevalent muni bond tax equivalent yield calculation in Figure 5:

Figure 5: Prevalent Municipal Bond Tax Equivalent Yield Calculation

Tax equivalent yield = Municipal bond yield / (1-investor's marginal tax rate)

There are two key flaws in this formula. First, since it seeks to determine the pre-tax yield needed by a taxable bond to offer the same after-tax return of a municipal bond, it assumes we are comparing like-for-like bonds. As discussed above, municipal bonds and investment grade corporate bonds have vastly different call provisions, whereby muni bond interest income can disappear many years before maturity.

Bondsavvy Subscriber Benefit

Through Bondsavvy's active investment strategy, we update our corporate bond recommendations each

quarter based on issuer financials and bond pricing metrics. Our goal is to

maximize total returns for each investment recommendation.

Get Started

As shown in Figure 1, the median bond in our search of municipal bonds with August 2044-August 2046 maturities was subject to a par call 11 years before maturity. A municipal bond with this call provision is not comparable to a 20-year investment grade corporate bond that has a make whole call.

Second, what "yield" are we talking about in the formula's numerator? Most investors, as noted above, would assume "municipal bond yield" means yield to maturity; however, yield to maturity includes the return from interest income plus expected capital gain or minus expected capital loss. Since the municipal bond tax exemption only pertains to the bond's income, including the capital gain portion of the YTM for bonds priced at a discount to par value overstates the bond's tax equivalent yield, as muni and corporate bond capital gains are taxed at similar rates.

To illustrate our point further, Figure 6 shows two municipal bonds and two corporate bonds, all of which mature in 2035. On August 21, 2025, the Harris County, TX '35 bond had a YTM of 4.38% and a current yield of 2.45%, as discussed above. The current yield shows a bond's annual income return assuming no change in the price of the bond.

Figure 6: Sample Municipal and Corporate Bond Taxable Equivalent Yield Comparison -- August 21, 2025

| First Par Call

Date | Bid

Price | Offer

Price | Yield to

Maturity (YTM) | Current

Yield | Current Yield

TEY* |

|---|

| Sample Municipal Bonds | | | | | | |

Harris County, TX Dept of Ed. 2.00% 2/15/35

CUSIP: 414015DA2 | 2/15/30 | None | 81.72 | 4.38% | 2.45% | 3.22% |

Tampa, FL BayCare Health System 3.125% 11/15/35

CUSIP: 87515EBY9 | 5/15/26 | None | 89.50 | 4.41% | 3.49% | 4.59% |

| | | | | | |

| Sample Investment Grade Corporate Bonds | | | | | | |

Waste Management 3.90% 3/1/35

CUSIP: 94106LBB4 | 9/1/34 | 91.81 | 92.10 | 4.95% | 4.23% | 4.23% |

Honda Motor Co. 5.337% 7/8/35

CUSIP: 438127AF9 | 4/8/35 | 100.56 | 100.80 | 5.23% | 5.29% | 5.29% |

Sources: Fidelity.com and Bondsavvy calculations. * "TEY"= taxable equivalent yield. Assumes 24% US federal tax bracket and no state income tax. For 2025, the 24% married filing jointly tax bracket was for incomes between $206,700 to $394,600.

Figure 6 shows real-life examples of municipal bonds with par calls long before maturity. The Harris County '35 bond is callable at par five years before maturity, and the Tampa, FL '35 bond is callable at par 9.5 years before maturity. That said, since these bonds have low coupons, they do have lower call risk than higher-coupon municipal bonds.

An alternative taxable equivalent yield calculation

As noted above, a significant portion of the Harris County, TX '35 bond's YTM accounted for capital appreciation between August 21, 2025 and the February 15, 2035 maturity date of approximately 18 points. Therefore, if we used the bond's 4.38% yield to maturity in the tax equivalent yield calculation, we would vastly overstate the bond's tax equivalent yield.

Instead, the true taxable equivalent yield should be based on the Harris bond's current yield of 2.45%, which, assuming a 24% federal income tax rate and no state income tax in Texas, provides a 3.22% current-yield-based taxable equivalent yield ("CYBTEY"). This is well below the current yields offered by the two sample corporate bonds: 4.23% for the Waste Management 3.90% '35 bond and 5.29% for the Honda Motor 5.337% '35 bond. If we then added 1.93% to the 3.22% CYBTEY for the Harris '35 bond, we would arrive at an adjusted taxable equivalent yield of 5.15%, which is between the August 21, 2025 YTMs of the Waste Management '35 and Honda Motor '35 bonds.

Of course, this is just the yield to maturity and current yield. Earlier in this fixed income blog post, we discussed the greater certainty of income and higher capital appreciation opportunities corporate bonds can provide when compared to municipal bonds. In our view, these factors can enable corporate bonds to achieve higher long-term investment returns than municipal bonds.

Bondsavvy has shown how an active bond investment strategy can enable investors to achieve corporate bond returns that exceed a bond's purchase date yield to maturity. Through August 1, 2025, for the 78 corporate bond recommendations Bondsavvy had exited, we achieved a 10.11% median annual return, exceeding the pick date yields to maturity of these previously recommended bonds, significantly in many cases.

Conclusion

The old way of calculating municipal bond tax equivalent yields ignores key differences between corporate and municipal bonds and between bonds that are priced at different levels relative to par value. For bonds trading below par value, we believe it's important to use our CYBTEY calculation to ensure the tax equivalent yield is not overstated. In addition, if a muni bond's adjusted tax equivalent yield and a corporate bond's YTM are similar, in many cases, the corporate bond will have the advantage. This is due to their more favorable corporate bond call provisions and how these maximize income security and potential capital appreciation.

Of course, this analysis is not intended to say there are not cases where select municipal bonds could work for certain investors, including investors in higher tax brackets and in states with high income taxes. In addition, not all municipal bonds are callable at par well before maturity.

This fixed income blog posts seeks to encourage investors to dig deeper into the terms of the bonds they invest in rather than relying on a standardized formula that, more often than not, is irrelevant and misleading.

** Based on a Fidelity.com bond search Bondsavvy conducted on August 21, 2025, which included 1,520 municipal bonds maturity from August 2044 to August 2046.

Bondsavvy does not provide tax advice or any individualized advice.

Get Started

Watch Free Sample